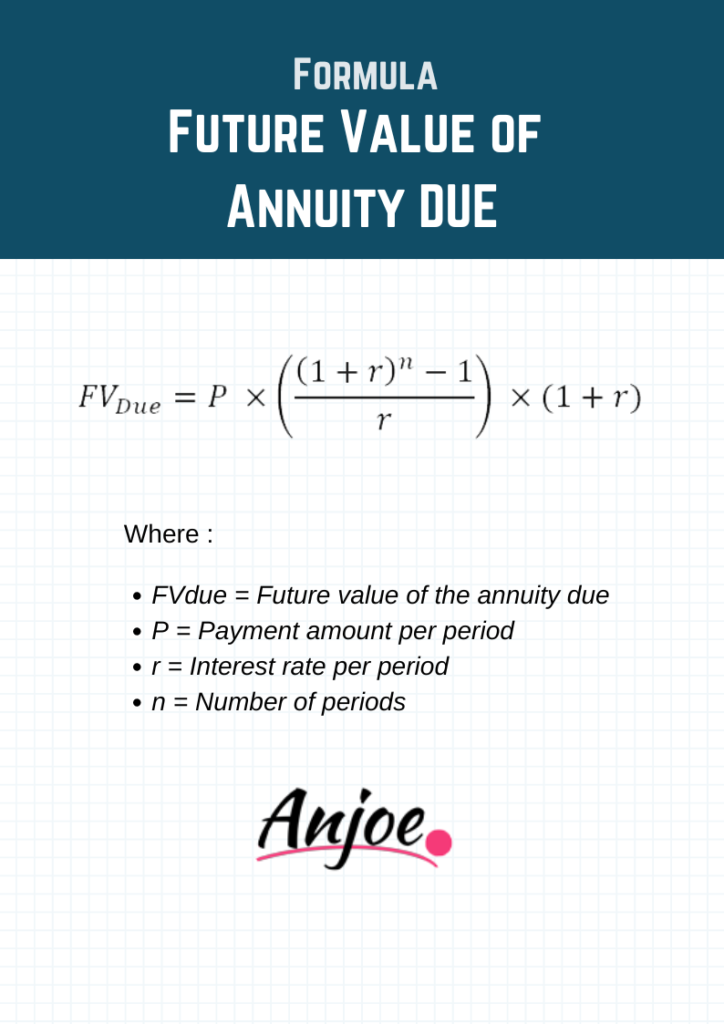

To calculate the future value of an annuity due, we need to adjust the formula for the future value of an ordinary annuity to account for the fact that payments are made at the beginning of each period rather than the end.

Future Value of Annuity Due Calculator

This formula accounts for the fact that each payment is invested for one additional period compared to an ordinary annuity.

The concept of annuities is pivotal for both investors and individuals planning their retirement. Among the various types of annuities, the “annuity due” is a fundamental concept, particularly for those looking to understand the growth of regular investments made at the beginning of each period. This article delves into the intricacies of the future value of an annuity due, explaining its significance, formula, and practical applications.

What is an Annuity Due?

An annuity due is a series of equal payments made at regular intervals, with each payment occurring at the beginning of the period. This differs from an ordinary annuity, where payments are made at the end of each period. Common examples of annuity due include lease payments, insurance premiums, and certain types of pension plans.

Importance of Calculating the Future Value

The future value (FV) of an annuity due is the total value of a series of payments at a specified point in the future, accounting for a certain interest rate. This calculation is crucial for several reasons:

- It helps individuals estimate how much their regular contributions to a retirement plan will grow over time.

- Investors can use it to evaluate the potential growth of their investments when payments are made at the beginning of each period.

- Businesses can forecast the future value of regular expenses or revenues that occur at the start of each period.

Practical Example

Consider an individual who contributes $1,000 at the beginning of each year to a retirement account with an annual interest rate of 5%, for 10 years. Using the formula:

Thus, the future value of the annuity due after 10 years would be $13,206.

I genuinely enjoy studying on this site, it has great posts.

Thank you for your feedback